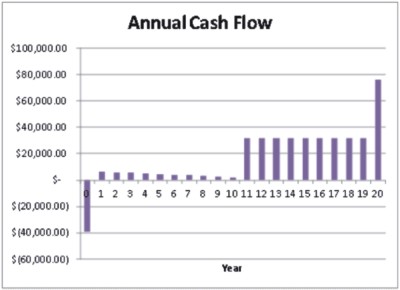

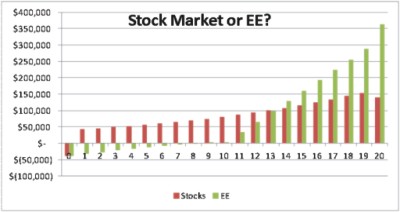

Last week we looked at the financial benefits of energy efficiency as compared to the stock market. I’m going to take this a few steps further, as forewarned last week.In both cases we start with the $39,000 investment and the stock market simply grows at its long-term average of 7.5% (Dow Jones Industrials). Obviously, a smooth appreciation of your investment is not the case and if you don’t have a strong stomach, you should avoid equities. Why is it called the Dow Jones Industrial Average anyway? It’s full of service companies, banks, and retailers. It includes Microsoft, but not Apple,…

Read More